Overview

This idea came from an auto ride. I overheard the driver saying he was struggling to arrange just ₹2,000 to go home after his mother passed away. That moment stuck with me—and made me realize how often daily wage workers in India face the same helplessness.

People like auto drivers, maids, and delivery workers usually don’t have credit history or salary slips—so they’re locked out of formal loans. In tough times, they’re forced to borrow from friends or fall into debt traps.

Paytm being the most used UPI app among gig workers, I designed a microloan feature offering quick, low-interest emergency loans with no paperwork and no credit score. Just simple, ethical support when they need it most.

My Role

Product Designer — Product Strategy, User Research, UX Flow Mapping, Prototype Design

Duration

2 weeks- May 2025

Tools Used

Figma, FigJam, Notion, Miro

With the population of gig workers in India being over 25 million, If even 1 lakh users adopt this microloan feature monthly, Paytm can earn:

₹15 Crores +

Revenue per month

₹180 cr

Yearly revenue

By combining empathetic design with business growth, this feature proves that profit and purpose can go hand-in-hand.

Why it matters?

Paytm Microloan Feature

Personal project

10 min read

Design

Process

Introduction

A moment in an auto ride sparked this idea…

“Just give me ₹2,000… my mother has passed away and I need to go back to my village."

That’s what the auto driver pleaded over the phone as I sat quietly in the backseat. His friend asked him to give up his auto in return—his only source of income. The driver hung up in tears.

Auto drivers, maids, gig workers, and other informal sector workers rarely have access to formal credit. In moments of crisis, they’re often forced to borrow from friends or fall into the traps of predatory moneylenders.

It made me wonder:

What if there was an option, where people like him could get micro/mini loans for such emergencies?

Problem

Millions can’t get help when they need it most

Current systems are built for salaried users, ignoring everyone else.

According to Niti Aayog, by 2030, India’s gig economy is projected to grow to over 25 million workers, yet a majority of these workers remain financially invisible to the formal banking system. With no fixed salary, no collateral, and often no credit history, nearly 70% of gig workers are denied personal loans by traditional institutions.

At the same time, most digital lending platforms—including Paytm—only offer loans starting at ₹10,000, often requiring formal employment or credit scores. But people living paycheck to paycheck don’t need ten thousand. They need small amounts money urgently and efficiently with re-payable interest rates.

User Flow

Crafting a smooth pathway for users

Ideation techniques I Explored

I made a series of “How Might We” questions and then split them into sections by importance

Now you might be wondering…can Paytm use its own ecosystem data to offer fair microloans?

Yes. Here’s how this idea holds up across three pillars of product innovation:

Define

A Microloan That Meets You Where You Are

Problem Statement

Dinesh, an auto driver with unpredictable income, needs access to small, reliable emergency loans to manage sudden expenses which cant be delayed without facing rejection, fraud or emotional burden.

Goal Statement

Our microloan feature in Paytm will let users like Dinesh apply for and receive small, reliable emergency loans instantly, which will affect low-income workers with unpredictable earnings by reducing their financial stress and giving them access to funds without emotional burden or rejections. We will measure effectiveness by tracking how many users apply for the loan.

Solution

How I met these high priority challenges

I brainstormed once again for all the features and possibilities that would be best both for Paytm and my users.

To solve the most urgent challenges, I focused on ideas that fit smoothly into Paytm's existing system and truly helped people like Dinesh. Every choice balanced what was practical for the product and what felt right for the user. I looked for the simplest actions the user could take and the easiest data Paytm already had—so things would feel fast, clear and safe.

I prioritized speed, trust, and accessibility—without compromising business viability. Here’s how I approached it:

No CIBIL / credit history?

— Use SMS, wallet, UPI, and Paytm transaction data as alternate signals of creditworthiness.

Fast, simple process

— Short form, auto-filled details, minimal KYC

Use Paytm ecosystem

— Background check from wallet & UPI data

Alternative credit model

— Blend behavioral data with Paytm’s internal risk score to qualify more users fairly.

Build trust

— Explain clearly why users were accepted or not, ensure no hard rejections, and guide them gently to improve their eligibility.

UI design

Designing with Intent, Not Just Style

With no design system in place, I created a cohesive and scalable UI language.

Color Palette

With the color palette of Paytm already set, I simply followed those styles in the mobile app design. Their main color is a light blue and navy blue. It’s meant to convey trust, stability, and professionalism—qualities that match the app's brand image.

Typography

The font I chose is Roboto. It’s modern and easy to read, which works well across different devices.

Design Components

Without official brand guidelines, I crafted a design system inspired by Paytm’s visual identity. Buttons, cards, and layouts were built to feel native while improving usability and clarity.

Icons

I picked clean, recognizable icons to match Paytm’s tone. These icons guide users without overwhelming them, reducing cognitive effort.

Designs That Answered Real Needs

Each design choice started with a user insight or a gap in the market—here’s how I responded.

Problem: Loan application process was lengthy and frustrating

“I just want the money quickly—no long forms please.” - from interview

I created a 3-step loan process that’s fast and frictionless.

Users enter their details, take a selfie for KYC, and choose the loan amount — all in under 2 minutes.

Most platforms overwhelm users with lengthy forms, but this flow is simple enough to work even for less tech-savvy users and reduces drop-offs.

Problem: Most users had unstable incomes

"I barely get through the week with the money I earn" - shared by 96% of users.

I offered flexible repayment options and kept monthly interest rates below 4%.

This approach supports users with unpredictable incomes—like gig workers—helping them manage their finances without stress of repayment.

Problem: Users feared missing EMI due dates

I added a simple “Add to calendar” option and made upcoming EMIs clearly visible.

This helps users stay organized and avoid late payments—especially important for those juggling multiple responsibilities in their busy life.

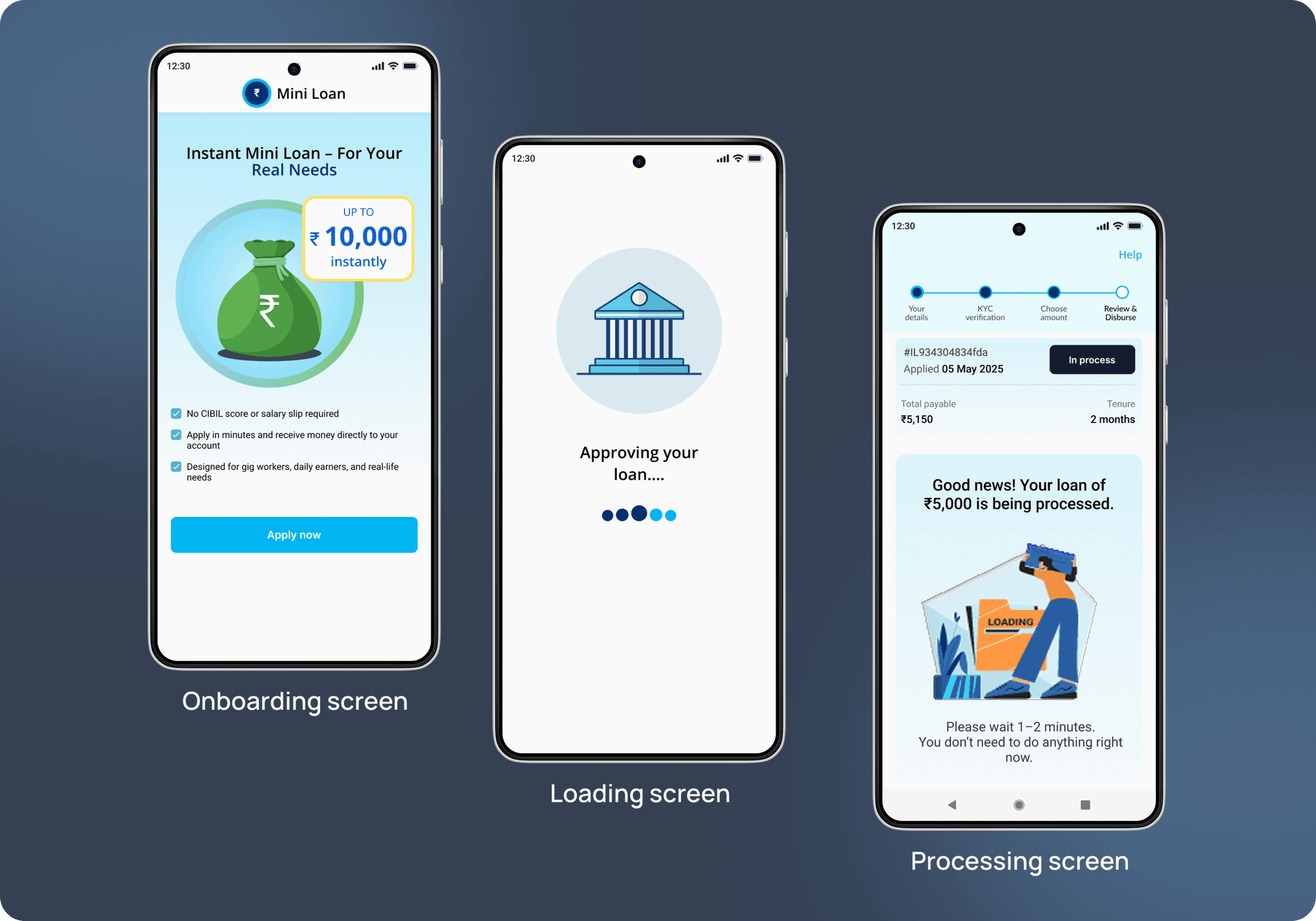

Other screens

These screens cover the in-between steps from approval to loading—keeping users informed, in control, and stress-free.

User groups

From the research, I identified two main user groups.

Digitally-Aware but Credit-Strained Workers

Age: 30–45

Auto drivers, small sellers, gig workers

Use Paytm, GPay, or PhonePe regularly

Have taken informal or formal loans

Want lower interest rates and flexible options

Would use Paytm loans if transparent and trustworthy

Older or Less Digitally-Aware Workers

Age: 45-55+

Security guards, maids, manual laborers

Avoid digital financial services

Hesitant or distrustful of online lending

Rely on family or cash savings

May use Paytm loans only in extreme emergencies if very simple and guided

I focused on the first group as they’re already digitally active and more likely to adopt the feature, while still making sure the design stays simple and trustworthy enough for the second group to use in emergencies.

To move beyond assumptions, I conducted qualitative interviews with daily wage earners such as auto drivers, security guards and small vendors.

Research

Process

Cute note-taking :)

But after quite some research the results were really shocking

"

"

💬 Goal: Understand how users handle emergencies, trust tech, and view online loan services

66%

don’t regularly use Paytm—but would consider it if it offered quick, low-interest emergency loans.

20%

expressed strong distrust in online loan services, showing that trust-building is non-negotiable.

20%

are regular Paytm users and said they would definitely use the feature if it offers better interest rates than banks.

15%

have never needed a loan before, signaling that while the market exists, onboarding and timing are key for adoption.

Key takeaways

Loan Experience is Not One-Size-Fits-All

Even though the need is urgent and real, today’s loan systems ignore the rhythm of gig and informal lives.

1) Paytm or Digital Trust Varies Greatly

Some users trust and regularly use digital platforms like Paytm, GPay, PhonePe.

Others—especially older users—avoid online services entirely.

2) Emergency Loans are a Real Need

Many have faced situations needing urgent funds (e.g., medical, personal issues).

Auto drivers especially turn to friends for loans, even against personal items (like gold), which brings emotional + financial stress.

3) High Bank Interest is a Barrier

Loans from banks come with high interest (8–12%) and long formalities.

Users feel a smaller, faster, lower-interest loan would be more helpful.

4) Flexibility in Repayment is Important

For a ₹5,000 loan, some said they’d need up to 4 months to repay.

Users value customizable repayment duration.

5) Loan Experience Level Varies

Some have never taken any formal loan before.

Others have taken high-value loans or borrowed informally from friends/family.

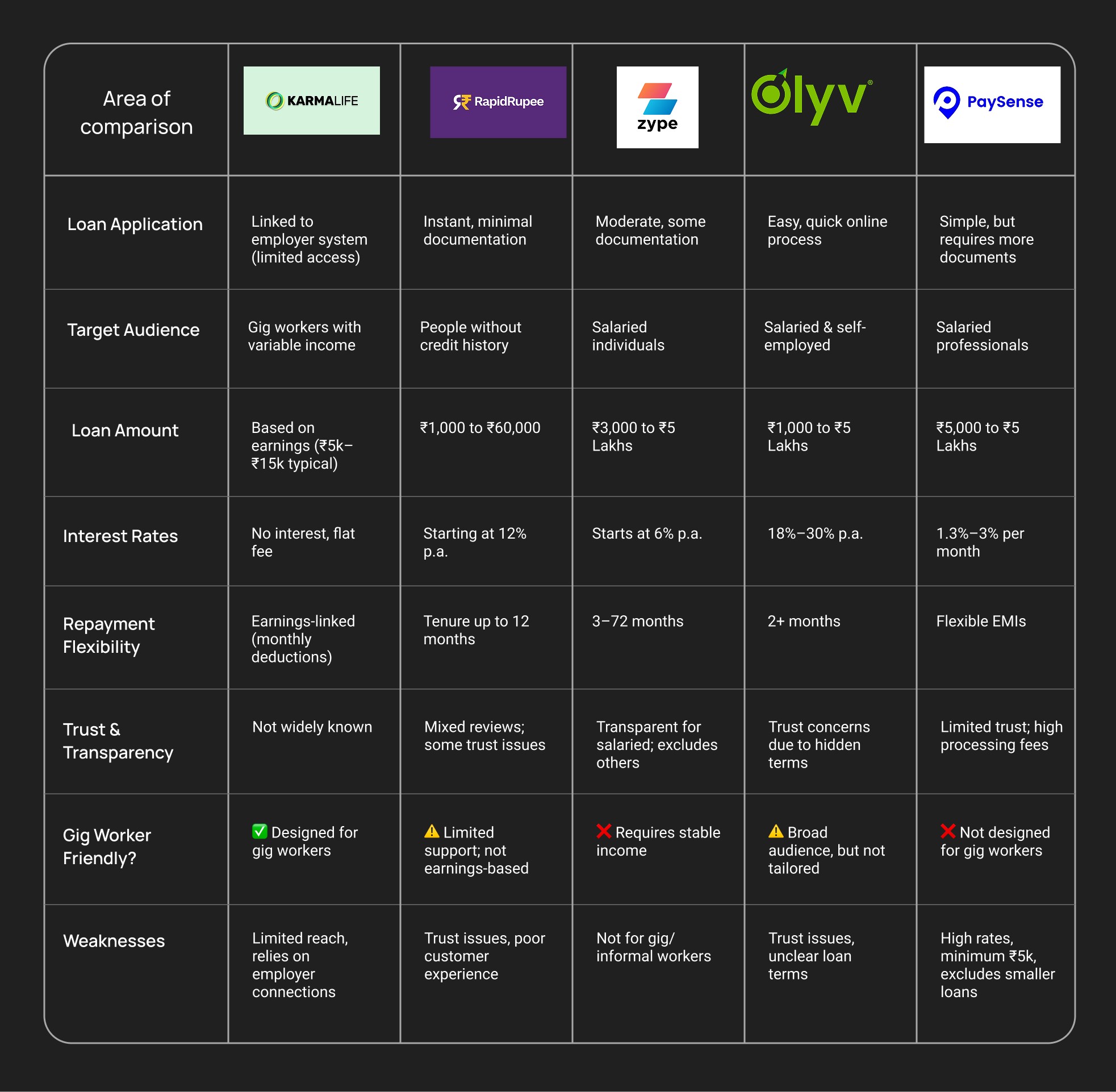

Competitive analysis

At first, I assumed there were no microloan apps offering quick, paperless loans under 10k rupees. But after digging deeper, I found many services do exist—each solving only a part of the puzzle.

That’s why I conducted an in-depth competitive analysis, focusing specifically on digital loan services that offer loans below ₹10k, claim to require minimal paperwork or verification and target users without formal employment or strong credit scores.

The goal was simple:

To uncover what’s working, what’s missing, and where Paytm could truly stand out.

Full report

Full report

Feature

Showcase

Interactive prototype

Testing report

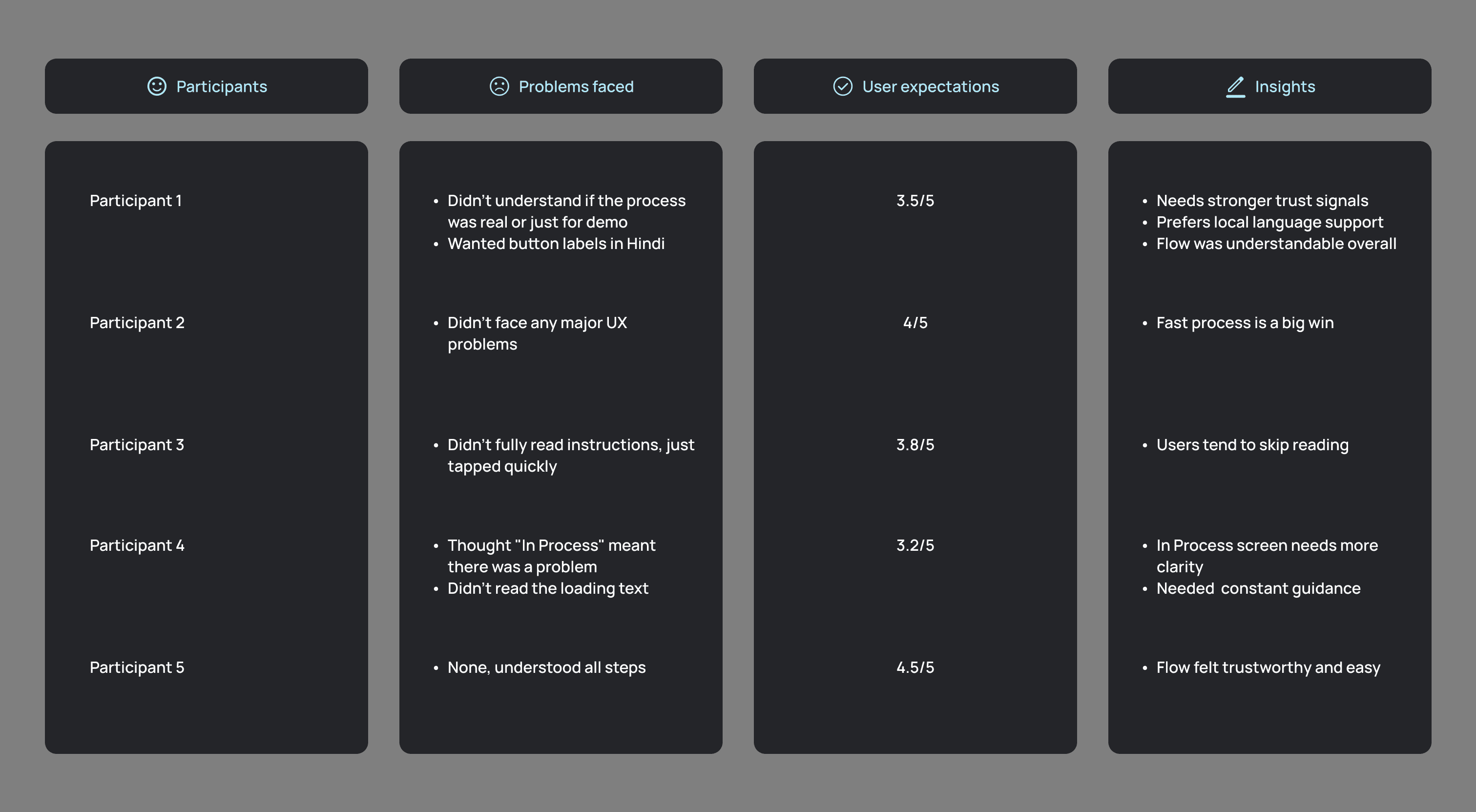

Usability Testing with Real Users

Understanding how first-time, low-literacy users interact with the microloan experience

Methodology:

5 participants (2 auto drivers, 2 delivery boys, 1 vegetable shop owner) were asked to complete the loan request flow using the prototype on a mid-range Android phone.

Goals:

Can users understand what’s happening on each screen?

Do they feel comfortable and confident borrowing money from this app?

Is the flow smooth and easy for them?

Can they easily read and understand the language used?

Iteration: Improved Processing Screen for Clarity

The problem:

Users with low digital literacy were confused by the "In process" screen. The language felt technical, and the visual didn’t clearly communicate what was happening.

Lessons learned

A feature with the power to change lives—and business outcomes.

This project reminded me how powerful design can be when it listens with empathy and moves with intention. I learned that:

It’s okay to start small if it solves a real problem well

The best UX is invisible—it just feels natural

Ethical design isn’t just about doing good. It can also drive real growth

By helping daily wage workers access instant, dignified financial support, this microloan feature has the potential to transform both lives and Paytm’s business.

With Paytm’s trust, reach, and low cost of digital delivery, this could become one of its most impactful, human-centered features yet.

Thank you!

If you made it this far, you are a real gem💎

Let’s chat — about design, gaming or anime. I’m all ears (and bows)! 💌💭

Made by Arohi with lots of love and sparkles ✨